A student in a probability course may have evaluated an integral such as the following:

Plug in a value for

The gamma function is denoted by the capital Greek letter

The Gamma Function

The starting point of the gamma function is that

As indicated above, the function gives the value of the factorial shifted down by one, i.e.

It is easy to evaluate

The recursive relation works for all real numbers

The idea can be extended further. For example, for any real number in the interval

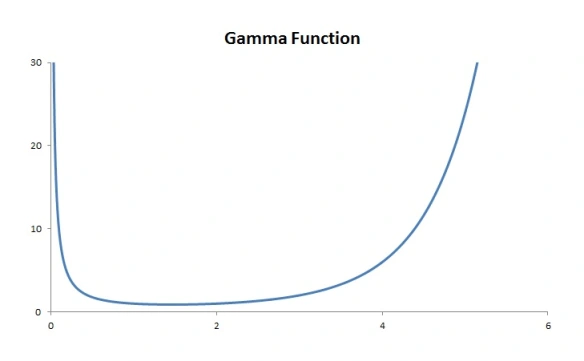

Gamma Function

The gamma function can also be extended to the complex numbers. Thus the gamma function is defined on all real numbers (except for zero and the negative integers) and on all complex numbers.

Gamma Distribution

We are now back to looking at the gamma function just on the positive real numbers

Let’s look at the graph of the integrand of the gamma function defined in (1). In particular, look at

Integrand of Gamma Function: area under curve is 24

The above graph is the graph of

Integrand of Gamma Function: area under curve is 1

Note that the graph of

where

where

The mathematical definition of the gamma distribution is quite simple. Once the gamma function is understood, the gamma distribution is clear mathematically speaking. The mathematical properties of the gamma function is discussed here in a companion blog. The gamma distribution is defined in this blog post in the same companion blog.

Beyond the Mathematical Definition

Though the definition may be simple, the impact of the gamma distribution is far reaching and enormous. We give a few indications. The gamma distribution is useful in actuarial modeling, e.g. modeling insurance losses. Due to its mathematical properties, there is considerable flexibility in the modeling process. For example, since it has two parameters (a scale parameter and a shape parameter), the gamma distribution is capable of representing a variety of distribution shapes and dispersion patterns.

The exponential distribution is a special case of the gamma distribution and it arises naturally as the waiting time between two events in a Poisson process (see here and here).

The chi-squared distribution is also a sub family of the gamma family of distributions. Mathematically speaking, a chi-squared distribution is a gamma distribution with shape parameter

This blog post discusses the chi-square distribution from a mathematical standpoint. The chi-squared distribution also play important roles in inferential statistics for the population mean and population variance of normal populations (discussed here).

The chi-squared distribution also figures prominently in the inference on categorical data. The chi-squared test, based on the chi-squared distribution, is used to determine whether there is a significant difference between the expected frequencies and the observed frequencies in one or more categories. The chi-squared test is based on the chi-squared statistic, which has three different interpretations – goodness-of-fit test, test of homogeneity and test of independence.Further discussion of the chi-squared test is found here.

Another set of distributions that are derived from the gamma family is through raising a gamma distribution to a power. Raising a gamma distribution to a positive power results in a transformed gamma distribution. Raising a gamma distribution to -1 results in an inverse gamma distribution. Raising a gamma distribution to a negative power not -1 results in an inverse transformed gamma distribution. These derived distributions greatly expand the tool kit for actuarial modeling. These distributions are discussed here.

The applications discussed here and in the companion blogs are just scratch the surface on the subject of gamma function and gamma distribution. One thing is clear, the one little integral in (1) above has a far and wide reach in mathematics, statistics and engineering and other fields.