We present more examples to further illustrate the thought process of conditional distributions. A conditional distribution is a probability distribution derived from a given probability distribution by focusing on a subset of the original sample space (we assume that the probability distribution being discussed is a model for some random experiment). The new sample space (the subset of the original one) may be some outcomes that are of interest to an experimenter in a random experiment or may reflect some new information we know about the random experiment in question. We illustrate this thought process in the previous post Conditional Distributions, Part 1 using discrete distributions. In this post, we present some continuous examples for conditional distributions. One concept illustrated by the examples in this post is the notion of mean residual life, which has an insurance interpretation (e.g. the average remaining time until death given that the life in question is alive at a certain age).

_____________________________________________________________________________________________________________________________

The Setting

The thought process of conditional distributions is discussed in the previous post Conditional Distributions, Part 1. We repeat the same discussion using continuous distributions.

Let

We assume that

Suppose that in the random experiment in question, certain event

Since the event

The above probability distribution is called the conditional distribution of

Once this new probability distribution is established, we can compute various distributional quantities (e.g. cumulative distribution function, mean, variance and other higher moments).

_____________________________________________________________________________________________________________________________

Examples

Example 1

Let

Suppose that you have just purchased a one such computer that is 2-year old and in good working condition. We have the following questions.

- What is the expected lifetime of this 2-year old computer?

- What is the expected number of years of service that will be provided by this 2-year old computer?

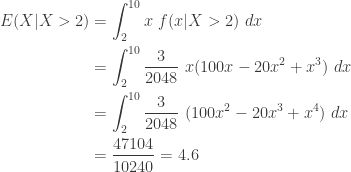

Both calculations are conditional means since the computer in question already survived to age 2. However, there is a slight difference between the two calculations. The first one is the expected age of the 2-year old computer, i.e., the conditional mean

For a brand new computer, the sample space is the interval

The conditional density function of

The first conditional mean is:

The second conditional mean is:

In contrast, the unconditional mean is:

So if the lifetime of a computer is modeled by the density function

Note that the following calculation is not

The above calculation does not use the conditional distribution that

Example 2 – Exponential Distribution

Work Example 1 again by assuming that the lifetime of the type of computers in questions follows the exponential distribution with mean 4 years.

The following is the density function of the lifetime

The probability that the computer has survived to age 2 is:

The conditional density function given that

To compute the conditional mean

Then

We have an interesting result here. The expected lifetime of a brand new computer is 4 years. Yet the remaining lifetime for a 2-year old computer is still 4 years! This is the no-memory property of the exponential distribution – if the lifetime of a type of machines is distributed according to an exponential distribution, it does not matter how old the machine is, the remaining lifetime is always the same as the unconditional mean! This point indicates that the exponential distribution is not an appropriate for modeling the lifetime of machines or biological lives that wear out over time.

_____________________________________________________________________________________________________________________________

Mean Residual Life

If a 40-year old man who is a non-smoker wants to purchase a life insurance policy, the insurance company is interested in knowing the expected remaining lifetime of the prospective policyholder. This information will help determine the pricing of the life insurance policy. The expected remaining lifetime of the prospective policyholder is called is called the mean residual life and is the conditional mean

In engineering and manufacturing applications, probability modeling of lifetimes of objects (e.g. devices, systems or machines) is known as reliability theory. The mean residual life also plays an important role in such applications.

Thus if the random variable

On the other hand, if the random variable

_____________________________________________________________________________________________________________________________

Summary

In conclusion, we summarize the approach for calculating the two conditional means demonstrated in the above examples.

Suppose

Then we have the two conditional means:

If

If

_____________________________________________________________________________________________________________________________

Practice Problems

Practice problems are found in the companion blog.

_____________________________________________________________________________________________________________________________